Founder Insight: The Four Killer De’s

In this exclusive guide, learn how and why decoupling, deglobalization, deindustrialization, and depopulation will define the next era.

Founder Insight: The Four Killer De’s

In this exclusive guide, learn how and why decoupling, deglobalization, deindustrialization, and depopulation will define the next era.

The last seventy-five years have been characterized by relative peace, which catalyzed rapid globalization, massive wealth creation aided by accommodative monetary policy, a population boom and incredible advancements in science, technology, and industry. The beginning of the end of that era is under way as we transition to a world marked by devolving geopolitical cooperation and the consequential acceleration of volatility, conflict, and risk. This era will be defined by depopulation and deindustrialization, which ultimately will lead to wealth destruction by way of persistent inflation, slower growth, capital flight and mass migration on an equally immense scale. While the leitmotif in the background will be consistent, the individual drivers behind this shift will fall within a few distinct genres that each merit their own individual exploration below.

This four-part series, written by our Founder, Brian C. Adams, sheds light on the “Killer De’s” seen in the market today.

1. Decoupling

Ian Bremmer, the distinguished president of the leading global political risk research and consulting firm, Eurasia Group, focused on “The Three Decouplings” in his most recent annual State of the World speech. The pivot from an interoperable global order to a disaggregated multimodal one will begin with a small number of large, high profile fissures that will eventually cascade across a fractured world.

China and the U.S.:

“[T]he pragmatism that allowed both China and America to profit enormously from globalization has broken down into acrimony and deep-seated distrust.”

The separation of the world’s two largest economies is accelerating at a breakneck pace. The reforms and trade deals of the 1990’s are relics of the past. Nationalistic political ideology now trumps capitalist motivations, with a focus on creating “Fortress China” to be immune to the type of economic pain being leveled on Russia at the moment in anticipation of an invasion of Taiwan. Meanwhile, the US has its own motivations to disentangle its supply chain, manufacturing and overall economy from China. The result on both sides is more regulation covering foreign investment, increased barriers to entry and more stringent oversight over companies with business interests in either country.

Russia from the West:

“It’s the most abrupt of the three. It’s also the most severe — and the most irreversible.”

Russia’s surreptitious invasion of Ukraine in an ill-conceived attempt to recover long lost imperial glory is the personification of this shifting geopolitical landscape we now occupy. A country suffering from horrendous demographics and a decaying industrial sector overly dependent on energy, their actions represent an outright rejection of the post-WWII global order, i.e., the US dominated NATO alliance and a pronounced about face to staunchly anti-US regimes in China, Iran and North Korea.

The West and Global South (developing countries):

“[P]oorer countries are less well prepared to limit (this) harm…That’s especially true in South Asia, North Africa, and the Middle East … and in Central America, a region already plagued with poverty and violent crime.”

As security conditions deteriorate across the world, countries with access to energy, natural resources, industries, and diversified economies will become increasingly insular and realign themselves along regional strategic coalitions. In a world of limited resources, domestic energy and food security will take priority over nebulous foreign mandates such as peacekeeping (UN) and debt bailouts (IMF).

According to a study by the IMF, “China contributed 28 percent of GDP growth worldwide – more than twice the share of the US.”

Given recent developments, the continuation of the Zero Covid policy and GDP forecasts, a contribution near that level in the future seems highly improbable. After generations of expending precious blood and treasure and having finally secured energy independence, it is clear America no longer has the political will or appetite to police the world. This power vacuum, exacerbated by the fallout from COVID and war in Europe, widens the gap of the haves and have-nots and places the modern global system, itself, on the verge of fragmentation.

2. Deglobalization

How did we get here?

The free flow of ideas, people and capital across the globe under the aegis of American leadership and patronage after the Second World War, ushered in a golden era of globalized commerce and interconnectedness characterized by a precipitous decline in the cost of moving goods, a reduction of trade barriers and tariffs, technological wizardry and a frenetic liberation of the world’s financial system. The fall of the Berlin Wall followed shortly thereafter by China, Russia and India opening their borders supercharged international travel, communication and business activity.

Investors benefited hugely as multinational corporations expanded into developing markets, unlocking untapped demand for new products, lower labor costs, as well as cheaper natural resources and raw materials. Larger markets and lower input costs for companies increased global competition, which drove down prices and created a larger variety of choices for consumers.

International and super regional organizations, such as the United Nations, World Trade Organization, International Monetary Fund, NATO and EU, were seen as the conditions precedent and the bulwarks to achieving and maintaining the international peace and security necessary for this miracle of commerce.

Why did it end?

The Great Financial Crisis of 2008 marked the beginning of the end of this gilded age. Brexit, the Trade Wars of the Trump administration, the pandemic, war in Ukraine, supply chain breakdowns, the rise of populism and China’s pivot to economic insularity, have compounded on one another such that the go-go days of hyper globalization have given way to a malaise of economic torpidity and seen the grand edifices of the aforementioned, intergovernmental institutions fade into obsolescence.

The alphabet soup of global integration metrics used by economists are all either stagnant or in retreat relative to world GDP – including trade, cross-border investment, cross-border bank loans, capacity of supply chains, intermediate imports, multinational firm’s share of global profits and foreign direct investment.

What happens next?

As Adam Posen, President of the Peterson Institute for International Economics, puts it, this “corrosion of globalization” will reorient the world stage to regionalism: “It now seems likely that the world economy really will split into blocks, each attempting to insulate itself from and then diminish the influence of the other.”

What does a deglobalized world look like?

- Heightened political risk arising from weak intuitions such as the EU, tensions over unilateral trade imbalance, and lack of trust in China and Russia in their respective spheres of influence.

- Increased risk to a global financial system dominated by the dollar, the Fed and Wall Street where the US is no longer the de facto economic leader.

- A multipolar world of regional super powers means countries that are not part of large trading blocs will either be caught in the middle or left behind. This will disproportionately impact poor countries with scarce financial and natural resources that lack diversified economies.

- A surge in prices and an increase in domestic jobs.

- A rise in military spending.

The closest historical parallel to the age of globalization is the Belle Époque that occurred between 1871–1880 and the outbreak of World War I in 1914. It was an era characterized by optimism, regional peace, economic prosperity, colonial expansion, and technological, scientific, and cultural innovations.

The question is: Will our emerging period be defined by massive conflict, wealth destruction and chase as it was last century?

3. Deindustrialization

What are we talking about here?

- The British economist Alexander Cairncross has posited three characteristics of deindustrialization:

A straightforward long-term decline in the output of manufactured goods or in employment in the manufacturing sector. - A shift from manufacturing to the service sectors, so that manufacturing has a lower share of total employment. Such a shift may occur even if manufacturing employment is growing in absolute terms.

- That manufactured goods comprise a declining share of external trade, so that there is a progressive failure to achieve a sufficient surplus of exports over imports to maintain an economy in external balance.

Is it good or bad?

The answer is yes…

The good.

While most readers will feel a tinge of negativity at first blush of hearing the term (think the decline of the auto industry across the Rust Belt in the 1980’s), deindustrialization is not inherently a negative phenomenon.

On a global, macroeconomic level, it is a natural outcome in successful economies due to the maturation of industry and application of technology, which has greatly accelerated the growth of productivity in manufacturing. To wit, per a study conducted by the IMF, “during the past 25 years, employment in manufacturing as a share of total employment has fallen dramatically in the world’s most advanced economies.”

The bad.

On the other hand, acute periods of hyper-deindustrialization is a zero-sum proposition. Manufacturing and heavy industry is still a large piece of the economic pie (~ 16% of global GDP) and the disruptive themes of decoupling, deglobalization and depopulation will result in a binary outcome of winners and losers.

An example:

Look at what is happening in Germany. An economic business model dependent on cheap Russian energy and abundant demand from consumers in China is under severe pressure. German chemical giant BASF has announced it would permanently downsize its operations due to persistently high energy prices.

“The challenging framework conditions in Europe endanger the international competitiveness of European producers and force us to adapt our cost structures as quickly as possible and also permanently,” BASF Chief Executive Martin Brudermüller.

- ArcelorMittal SA, one of the world’s largest steelmakers, will close a blast furnace in Bremen and a so-direct reduction plant in Hamburg that produces crude steel. “You have to reinvent the whole energy supply chain on the go,” said Reiner Blaschek, chief executive of the company’s German business.

- “We need immediate emergency aid now, otherwise we are threatened with deindustrialization in Germany,” said Franziska Erdle, WV Metalle’s general manager.

- “Hakle GmbH, a German toilet-paper and hygiene-product maker this month declared itself insolvent and sought protection from creditors because it could no longer raise prices enough to offset higher paper costs due to energy prices.” – WSJ

The US is the direct beneficiary of this dynamic as firms look to relocate resources to a country with stable energy prices and protected supply chains.

4. Depopulation

Of all the “Killer De’s” I have discussed to date, no force will be as impactful and widespread as depopulation. Indeed, our shrinking populace is a primary driver behind the decoupling, deglobalization and deindustrialization I have commented on previously.

Wait, I thought we had too many people on earth?

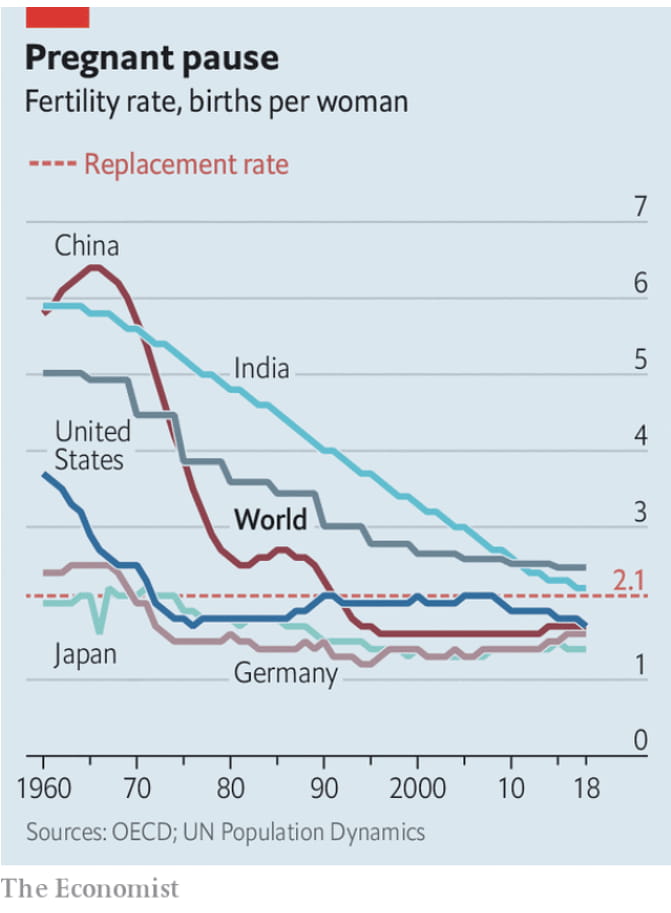

In contrast, to the dire prognostications in the 1960’s of a massively overpopulated and famine-stricken world, we now face a stark reversal in circumstances as we pivot from decades of dramatic global population growth to the sudden onset of precipitous population decline.

In addition to the demographics trends of a rapidly aging baby boomer generational cohort, per the Economist, “nearly half of the world’s people live in countries with fertility rates below replacement level (2.1 children per woman).”

In 1950 there was an average of 5 births per woman worldwide. Today it is 2.3 and the trendline is nosediving.

So, isn’t that a good thing?

A smaller population is certainly a positive factor in the context of a finite planet with limited resources facing environmental stress. Slower population growth also means increased opportunity for groups who have been historically underrepresented in the economy such as women and minorities. It also exerts upward pressures on wages, especially for unskilled labor, and theoretically raises productivity on a per worker basis.

On the other hand…

The few upsides are dramatically outweighed by the long-term negative economic implications. Demographics is the engine that drives growth so, by definition, declining labor forces and aging populations will experience slower, and, in some cases, contracting economies.

The same statistical superpowers that deliver exponential growth also drive exponential shrinkage on the other side of the tipping point.

Academics argue when exactly that time will arrive on a global scale, but there is no denying it is coming in the next few decades. Forty-six countries around the world, including major powers like Japan, Russia and China, now have shrinking populations. This number is projected to rise to 67 countries by 2040.

A few numbers to contemplate using China as a proxy:

- This month the National Bureau of Statistics announced China’s population fell by 850,000 in 2022 to ~1.4 Billion (the first decline in 60 years).

- The UN projects that China’s population will fall to 1.3 Billion by 2050 and 767 Million by the end of the century.

- Projections for 2040 show China’s working-age population falling by 114 million.

So what are the takeaways and consequences we need to be aware of?

- If fewer workers enter the labor force in the wake of falling fertility rates, while more older workers leave the labor force via retirement, the workforce will shrink and GDP per capita will be reduced.

- A scarcity of care workers is already stressing healthcare systems as baby boomers age.

- The fiscal math just doesn’t work for large social programs like Social Security, Medicaid and Medicare that are dependent on funding paid for by taxes derived from future working-age adults (The size of the working age population in the US has been stagnant for the past 15 years and set to decline this decade).

- Maintaining adequate investment spending to achieve optimal employment gets tricky when a lack of workers disincentives building new factories, housing, infrastructure, etc. Economists refer to this circumstance as “secular stagnation.”

- The sustainability of our government debt load comes into serious question (and if you worry about the solvency of the US, avert your eyes from the grotesque capital structures in third world and emerging markets, especially now that Russia, China and Iran are no longer viable debt sources).

- Fertility rates tend to be persistent and governmental schemes to reverse them are ineffectual, which means government fiscal, monetary and immigration policy will have to adapt accordingly.

It is important to reinforce the notion that the single best gauge of economic growth is growth in GDP per person, not total GDP.

GDP per capita is a rough proxy for average living standards. In theory, a country can increase its average living standard even though its population growth is low or even negative. It is just a matter of how quickly a decrease in population occurs.

So there is certainly hope to maintain our current lifestyles but, as in the previous missives I have written, there will be winners and losers in this new age.

A depopulating world characterized by slower growth, persistent inflation and a higher cost of capital will be a huge challenge for economic and social systems globally. Only countries with cohesive federal policies, effective immigration strategies and a commitment to invest heavily in technological advancements will be able to maintain and grow GDP per capita and avoid structural collapse and civil unrest.

Previous Articles

Excelsior Capital

A real estate private equity firm that owns and operates high quality multi-tenant office assets in emerging secondary markets.

Interested in learning more about Excelsior's investment opportunities?

Company

Investors

Excelsior Capital

104 Woodmont Blvd, Suite 120

Nashville, TN 37205

investors@excelsiorgp.com

Disclaimer: Under no circumstances should any information presented on this website be construed as an offer to sell, or solicitation of an offer to purchase any securities or other investments. This website does not contain the information that an investor should consider or evaluate to make a potential investment. Other materials related to investments in entities managed by Excelsior Capital are not available to the general public.